Complete Guide to All

Payment Systems in India

RTGS · NEFT · IMPS · UPI · NACH · BBPS · NETC · AePS · CTS · TReDS · PPI · Cards — What they are, how to use them, who controls them, and when to use each one.

Overall Regulator

Retail Payment Operator

(Banks, Fintechs)

📋 Table of Contents

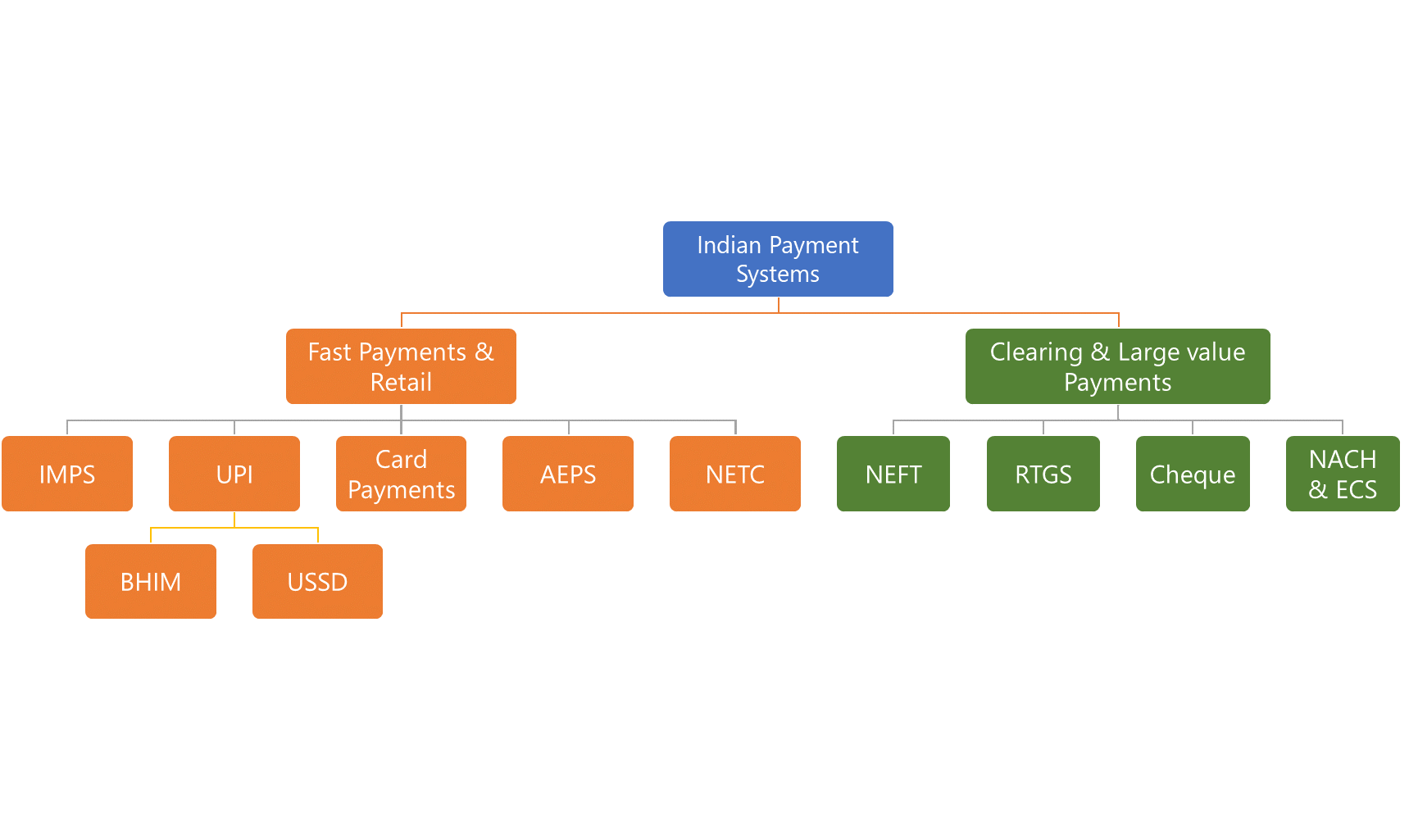

🗺️ India’s Complete Payment Ecosystem — At a Glance

The diagram below shows all players in India’s payment ecosystem — POS providers, Payment Gateways, Card Networks, Acquirer Banks, Issuer Banks, UPI PSPs, and POPs — all regulated by RBI & NPCI.

India’s complete payment ecosystem with all key players across categories

🇮🇳 India’s Payment Ecosystem — Introduction

India has one of the world’s most comprehensive and advanced digital payment ecosystems — regulated by the Reserve Bank of India (RBI) under the Payment and Settlement Systems Act, 2007. The actual operation of most retail payment systems is handled by NPCI (National Payments Corporation of India), set up in 2008 as a joint initiative of RBI and the Indian Banks’ Association (IBA).

From sending ₹10 via UPI to a tea seller, to transferring ₹100 crore via RTGS for a corporate deal, to paying your electricity bill via BBPS, to an Aadhaar-based cash withdrawal in a remote village — every digital rupee flows through one of India’s 12 major payment systems.

RTGS

High-value, real-time

NEFT

Retail fund transfer

NACH

Bulk auto-payments

IMPS

24×7 instant transfer

UPI

Smartphone payments

BBPS

Bill payments

NETC

FASTag toll payments

AePS

Aadhaar-based banking

CTS

Cheque clearing

TReDS

MSME invoice financing

PPI

Prepaid instruments

Cards

Debit & Credit cards

RTGS — Real-Time Gross Settlement

India’s Large-Value Payment System for instant high-value transfers

RTGS is India’s flagship large-value payment system — owned and operated directly by the Reserve Bank of India. The word “Gross” means each transaction is settled individually (not in batches), and “Real-Time” means it happens instantly. As of December 2020, RTGS operates 24 hours a day, 7 days a week, 365 days a year — making India one of very few countries with 24×7 RTGS. In 2024, RTGS processed 29.53 crore transactions worth an extraordinary ₹1,938.21 lakh crore.

📋 What is RTGS?

- Stands for Real-Time Gross Settlement

- Settlement happens instantly — one transaction at a time

- Used for large value transfers (minimum ₹2 lakh)

- No maximum limit — ideal for crore-value transactions

- Transactions are final and irrevocable once sent

👤 Who Uses RTGS?

- Businesses paying suppliers or vendors (high value)

- Corporates making bulk payroll (via bank)

- Property buyers — real estate transactions

- Importers/exporters for trade payments

- Loan repayments of large amounts

- Investment transactions above ₹2 lakh

📱 How to Use RTGS

- Log into your bank’s internet banking or mobile app

- Go to Fund Transfer → RTGS

- Add beneficiary: Name, Account No., IFSC Code

- Enter amount (minimum ₹2 lakh)

- Authenticate with OTP and confirm

- Money reaches in seconds (real-time)

- Also available at bank branch counter

💸 Charges & Limits

- Minimum: ₹2,00,000 (₹2 lakh)

- Maximum: No upper limit

- Inward transactions: FREE for receiver

- Outward transactions: Bank-decided charges (RBI removed its charges in 2019)

- Most banks charge ₹20–₹50 per RTGS transaction

NEFT — National Electronic Funds Transfer (Retail)

India’s most widely used electronic retail fund transfer system

NEFT is India’s most popular bank-to-bank fund transfer system for retail (everyday) transactions. Launched in 2005 and owned by RBI, it works on a Deferred Net Settlement (DNS) basis — meaning transactions are grouped into batches and settled 23 times a day in half-hourly intervals. As of December 2024, NEFT has 235 direct members and 1,928 sub-members, and processed 926.84 crore transactions worth ₹432.79 lakh crore in 2024.

📋 What is NEFT?

- Net settlement — transactions settled in batches

- 23 half-hourly batches run throughout the day

- Works 24×7×365 (since December 2019)

- Minimum: ₹1 | No maximum limit

- Requires recipient’s account number + IFSC code

- Slower than RTGS/IMPS but free for most customers

👤 Who Uses NEFT?

- Individuals transferring money to friends/family

- Small businesses paying vendors or employees

- EMI payments and loan repayments

- Utility bill payments via bank

- School/college fee payments

- Remittances to Nepal (Indo-Nepal Remittance, max ₹50,000)

📱 How to Use NEFT

- Login to net banking / mobile banking app

- Add beneficiary with Name, Account Number, IFSC Code

- Select NEFT as transfer mode

- Enter amount and confirm with OTP

- Funds settle in the next available half-hourly batch

- SMS/email confirmation received on settlement

- Available at bank branches too

💸 Charges

- RBI removed its charges to banks in July 2019

- Banks pass benefits to customers — mostly FREE online

- Branch NEFT: ₹2–₹25 per transaction (bank-specific)

- Inward NEFT: Always FREE for receiver

- No charge for NEFT via net banking at most major banks

How NEFT & RTGS transfer money: Sender → Sender’s Bank → RBI → Receiver’s Bank → Receiver (requires Account No. + IFSC)

NACH — National Automated Clearing House (Bulk Payments)

Automated bulk clearing system for repetitive, high-volume payments

NACH (National Automated Clearing House) is NPCI’s centralised electronic clearing system designed for bulk, repetitive, and periodic payments. It replaced the older ECS (Electronic Clearing Service) system and handles both one-to-many distributions (like government subsidy transfers to thousands of people) and many-to-one collections (like EMI deductions from lakhs of loan customers). This is what happens behind the scenes when your SIP is auto-debited every month or your salary arrives on time.

📋 Two Types of NACH

- NACH Credit (One → Many): Salary, pension, dividends, subsidies paid to many people

- NACH Debit (Many → One): EMI, insurance premium, SIP, utility bill auto-pay collected from many accounts

- Aadhaar Bridge Payment System (ABPS) is built over NACH for direct benefit transfer

👤 Who Uses NACH?

- Government: DBT (LPG subsidy, MGNREGA wages)

- Companies: Monthly salary disbursals to employees

- Banks: EMI auto-debit from loan customers

- Insurance: Premium auto-collection monthly

- Mutual Funds: SIP deduction every month

- Utilities: Electricity, telecom bill auto-pay

📱 How Does NACH Work?

- Customer gives a mandate (permission) once to auto-debit

- Mandate registered with bank via eNACH (online) or paper

- On scheduled date, amount auto-debited from your account

- You receive SMS/email confirmation of debit

- No manual action needed after mandate registration

IMPS — Immediate Payment Service (Fast Payments)

India’s 24×7 instant inter-bank payment system — the engine behind UPI

IMPS was India’s first 24×7 real-time inter-bank payment system, launched by NPCI in 2010. It was a revolutionary step — allowing instant fund transfers at any time, any day including holidays, using mobile phones. IMPS is notable because UPI is built on top of IMPS infrastructure. In 2024, IMPS processed 593.83 crore transactions worth ₹70.71 lakh crore. India was only the 4th country globally (after South Korea, UK, and South Africa) to launch such a payment system.

📋 What is IMPS?

- Instant, 24×7×365 inter-bank fund transfer

- Works via mobile, internet, ATM, SMS

- Transfer using mobile number + MMID, or account number + IFSC

- MMID = 7-digit Mobile Money Identifier issued by bank

- UPI runs on top of IMPS infrastructure

- Max limit: ₹5 lakh per transaction

📱 How to Use IMPS

- Via Mobile Banking: Enter amount + recipient mobile + MMID

- Via Net Banking: Enter account number + IFSC + amount

- Via ATM: Some banks allow IMPS from ATM

- Authenticate with MPIN or OTP

- Money credited instantly — even at 2 AM on holidays

💸 Charges

- Min: ₹1 | Max: ₹5,00,000 per transaction

- Most banks charge ₹5–₹25 per IMPS transaction

- Some banks offer free IMPS via app/net banking

- Costlier than NEFT for branch transactions

- UPI (which uses IMPS) is FREE for most transactions

UPI — Unified Payments Interface (Fast Payments)

India’s most transformative payment innovation — 50% of world’s digital transactions

UPI is NPCI’s most successful creation — a mobile-first, instant payment system that runs on top of IMPS infrastructure. Launched in 2016, it replaced the need to remember account numbers and IFSC codes with simple UPI IDs (like yourname@paytm). As of 2026, UPI accounts for 50% of the world’s real-time digital transactions — an extraordinary achievement. In 2026, UPI processed 228 billion transactions worth ₹300 lakh crore. It now works in 27+ countries globally.

📋 What is UPI?

- Mobile-first instant payment system by NPCI

- Links directly to your bank account — no wallet needed

- Pay using UPI ID / QR code / mobile number

- Built on top of IMPS infrastructure

- Regulated by RBI, operated by NPCI

- Works via apps: PhonePe, Paytm, Google Pay, BHIM, etc.

🚀 UPI Features 2026

- UPI Lite: Under ₹500 transactions without internet (offline)

- UPI 123Pay: Feature phones (*99# USSD)

- UPI for IPO applications (up to ₹5 lakh)

- Credit on UPI (credit line via bank linked)

- International UPI (27+ countries accepted)

- Bharat BillPay via UPI

📱 How to Use UPI

- Download any UPI app (PhonePe, Paytm, BHIM, etc.)

- Link your bank account using mobile number

- Create your UPI ID and set UPI PIN

- Pay by scanning QR, entering UPI ID, or mobile number

- Authenticate with 4/6 digit UPI PIN

- Money debited from your bank instantly

💰 Limits & Charges

- Standard P2P: ₹1 lakh per transaction

- IPO/NEFT/Education/Hospitals: ₹5 lakh per transaction

- UPI for P2P: FREE (no charges)

- UPI for merchants: FREE (no MDR for most)

- Market leader: PhonePe (48.3% share), Google Pay (37.6%)

UPI transaction flow: Payer initiates → PSP resolves VPA → UPI Server → Payee PSP → Banks debit/credit instantly

BBPS — Bharat Bill Payment System (Bill Payments)

India’s centralised, interoperable bill payment platform for all billers

BBPS (Bharat Bill Payment System) is India’s one-stop integrated bill payment platform — allowing any bill to be paid through any channel anywhere. Whether it’s electricity, water, gas, broadband, insurance, loan EMI, or FASTag recharge, BBPS connects all billers and all payment modes into a single, standardised system. In 2024, BBPS handled 217.47 crore transactions worth ₹7.68 lakh crore. NPCI created a dedicated subsidiary — Bharat BillPay Limited (NBBL) — in April 2024 specifically to manage BBPS growth.

💡 What Can You Pay via BBPS?

- Electricity bills (MSEDCL, BSES, BESCOM, etc.)

- Water and gas bills

- Broadband and DTH recharges

- Telephone (mobile postpaid, landline)

- Insurance premiums

- Loan EMIs and credit card bills

- FASTag recharge

- Municipal taxes and school fees

📱 How to Use BBPS

- Open any BBPS-enabled app (PhonePe, Paytm, CRED, bank apps)

- Select “Bills” or “Pay Bills” section

- Choose biller category (electricity, gas, etc.)

- Enter your consumer/account number

- Bill amount auto-fetched

- Pay via UPI, net banking, debit/credit card

- Instant confirmation and receipt

NETC — National Electronic Toll Collection (Toll Payments)

FASTag-based electronic toll collection system for highways across India

NETC is NPCI’s electronic toll payment system that uses FASTag — an RFID sticker on your vehicle’s windshield — to automatically deduct toll charges when you pass through a toll plaza. Since February 2021, FASTag became mandatory for all four-wheelers in India. In 2024, NETC processed 405.93 crore transactions worth ₹69.99 thousand crore — demonstrating how FASTag has transformed India’s highway experience by eliminating long queues at toll booths.

🛣️ How FASTag/NETC Works

- RFID sticker fixed on car/vehicle windshield

- Linked to your bank account or prepaid wallet

- When passing toll, RFID reader detects tag

- Toll amount auto-debited from linked account

- Barrier opens — no stopping, no cash exchange

- SMS alert received for every toll deduction

📱 How to Get FASTag

- Purchase from any authorized bank, NHAI toll plaza, or online (Amazon, Paytm)

- Attach to vehicle windshield (inside center-top)

- Link to bank account or load wallet (via PhonePe, Paytm)

- Recharge when balance is low via any UPI app

- Interoperable — one FASTag accepted at all toll plazas in India

- 20+ banks issue FASTags including SBI, HDFC, ICICI, Axis

AePS — Aadhaar Enabled Payment System

Banking for everyone — using only your Aadhaar number and fingerprint

AePS is one of India’s most impactful payment systems for financial inclusion. Launched in 2011, it allows any person with an Aadhaar-linked bank account to perform basic banking transactions using just their Aadhaar number and biometric fingerprint — no debit card, no PIN, no internet needed. This is revolutionary for rural India, where a villager can walk to a local Business Correspondent (BC/banking agent) and withdraw government subsidy money using just their thumb. In January 2024 alone, AePS handled 8.396 crore transactions worth ₹22,350.88 crore.

🆔 What Can You Do via AePS?

- Cash Withdrawal (withdraw from Aadhaar-linked account)

- Cash Deposit at Business Correspondent point

- Balance Enquiry (check account balance)

- Mini Statement (last few transactions)

- Fund Transfer to another Aadhaar-linked account

- Aadhaar-to-Aadhaar fund transfer

📱 How to Use AePS

- Visit a Business Correspondent (BC) / banking agent / micro-ATM

- Provide your 12-digit Aadhaar number

- Select bank name and transaction type

- Place your biometric fingerprint on the scanner

- UIDAI authenticates biometric, NPCI processes transaction

- Transaction completes — receipt printed or SMS sent

CTS — Cheque Truncation System (Cheques)

Modern digital cheque clearing — replacing physical movement of paper cheques

CTS is India’s electronic cheque clearing system that digitises the cheque clearing process. Instead of physically moving paper cheques from one bank to another (which took 2–3 days), CTS captures the cheque image and MICR data at the collecting bank and transmits it electronically to the paying bank. This dramatically speeds up cheque clearance from days to hours. CTS is mandated by RBI and covers the entire country through a grid-based clearing network.

📄 How CTS Works

- You deposit a cheque at your bank branch

- Bank scans cheque image + MICR data digitally

- Digital image transmitted to clearing house

- Clearing house sends to the paying bank electronically

- Paying bank verifies and credits/debits accordingly

- Physical cheque stays at collecting bank — not physically moved

📱 For Cheque Issuers/Receivers

- Cheque must be CTS-2010 standard compliant (most modern cheques are)

- Cleared same day or next working day

- Positive Pay System: For cheques above ₹50,000, inform your bank online

- Account Payee cheques cannot be endorsed to 3rd parties

- Don’t fold or staple cheques — damages image quality

TReDS — Trade Receivables Discounting System (MSME Financing)

Digital invoice financing platform — solving MSME cash flow challenges

TReDS is a specialised digital platform that solves one of India’s biggest MSME (Micro, Small & Medium Enterprise) problems — getting paid on time by large corporate buyers. A small supplier may have delivered goods to a large company but has to wait 90–180 days for payment. TReDS allows that MSME to upload its invoice and get it financed (discounted) by banks or NBFCs immediately — at a market-discovered interest rate. In 2024, TReDS processed 45.05 lakh invoices worth ₹1.69 lakh crore, of which 42.86 lakh invoices worth ₹1.60 lakh crore were financed. Monthly bill discounting has reached ₹17,000 crore.

🏭 How TReDS Works

- MSME delivers goods/services to a large corporate buyer

- MSME uploads the invoice on the TReDS platform

- Corporate buyer accepts/approves the invoice

- Banks/NBFCs bid to finance the invoice (factoring)

- MSME gets immediate payment (minus discount/interest)

- On invoice due date, corporate pays the financier directly

🏢 Who Can Use TReDS?

- MSMEs as sellers (UDYAM registered)

- Large corporations, PSUs, Govt. depts. as buyers

- Banks and NBFCs as financiers

- Three licensed TReDS platforms: RXIL, M1xchange, Invoicemart

- Reverse factoring (payables discounting) also available

PPI — Prepaid Payment Instruments

Digital wallets, gift cards, and prepaid cards — money you load before spending

PPIs are payment instruments that allow you to store money in advance and use it for purchases — like a digital pre-loaded purse. They include mobile wallets (Paytm Wallet, MobiKwik), gift cards (Amazon, Flipkart), prepaid cards (Visa/Mastercard prepaid), and meal/transit cards. PPIs are issued by banks and authorised non-bank entities (like Paytm Payments Bank) with RBI’s permission. They are categorised based on KYC and transaction limits.

💳 Types of PPIs

- Closed System PPI: Gift cards usable only at issuer’s store (Amazon, Flipkart gift cards)

- Semi-Closed PPI: Usable at multiple merchants (Paytm Wallet, MobiKwik)

- Open System PPI: Full card — ATM withdrawals allowed (Prepaid Visa cards)

- E-money wallets, prepaid debit cards, mobile wallets

📱 How to Use PPIs

- Load money into wallet via UPI/net banking/cash

- Use wallet at partner merchants for payments

- Min KYC wallet: Up to ₹10,000 balance

- Full KYC wallet: Up to ₹2,00,000 balance

- Gift cards: Use specific code at checkout

- PPIs linked to UPI can make UPI payments

How E-Money (PPI/Wallets) work: Money loaded from bank/card → stored in app → used for QR payments, wallet transfers, bank transfers

Cards — Debit & Credit Cards

India’s traditional payment instruments — RuPay, Visa, Mastercard, Amex

Cards remain one of India’s core payment instruments — both for online and offline transactions. India has three main card networks: RuPay (India’s own network by NPCI), Visa (American), and Mastercard (American). With 800+ million debit cards and growing credit card base, cards power everything from ATM withdrawals to online EMI purchases. NPCI’s RuPay card is specifically designed for India and now accounts for the majority of new debit card issuances, especially with its UPI integration (RuPay credit card on UPI).

🃏 Card Networks

- RuPay (NPCI): India’s own network — lower cost, works offline, UPI-enabled, government promoted

- Visa (USA): Largest global card network — accepted worldwide

- Mastercard (USA): Second largest global network — accepted worldwide

- Amex: Premium cards — accepted at select merchants

- Debit cards: Linked to your savings account

- Credit cards: Borrow now, pay later

📱 Card Payment Methods

- Swipe at POS terminal (physical shops)

- Insert EMV chip at terminal

- Contactless tap (NFC) — up to ₹5,000 without PIN

- Online: Enter card number, expiry, CVV + OTP

- ATM: Cash withdrawal using PIN

- RuPay credit card: Linked to UPI for mobile payments

📊 Step 1 — Card Authorization (Offline/POS)

When you swipe or tap your card at a shop, this is how the authorization happens in real-time:

Card authorization at POS: Customer swipes → POS → Acquiring Bank → Card Network (Visa/MC/RuPay) → Issuer Bank → Approval/Rejection

📊 Step 2 — Online Card Payment (Payment Gateway)

When you shop online and enter your card details, the Payment Gateway routes your transaction:

Online card payment flow: Customer enters card details → Payment Gateway → Acquiring Bank → Card Network → Issuer Bank → Approval/Rejection with OTP

📊 Step 3 — Card Clearing & Settlement

After authorization, the actual money movement (clearing & settlement) happens in batches:

Card clearing/settlement: Merchant captures transactions in batches → Acquiring Bank → Card Network verifies → Issuer Bank disburses funds → Merchant receives (minus fees)

📊 Complete Comparison — All 12 Payment Systems

| System | Controller | Launched | Speed | Min / Max | Availability | Best For |

|---|---|---|---|---|---|---|

| 🏛️ RTGS | RBI | 2004 | Real-time ⚡ | ₹2L / No limit | 24×7×365 | High-value corporate transfers |

| 📨 NEFT | RBI | 2005 | Batch (½ hr) | ₹1 / No limit | 24×7×365 | Everyday retail transfers |

| 🔁 NACH | NPCI | 2016 | Batch (day) | Varies | Business days | Salary, EMI, SIP auto-pay |

| ⚡ IMPS | NPCI | 2010 | Instant ⚡ | ₹1 / ₹5L | 24×7×365 | Instant transfers, UPI base |

| 📱 UPI | NPCI | 2016 | Instant ⚡ | ₹1 / ₹1-5L | 24×7×365 | Daily mobile payments |

| 💡 BBPS | NPCI/NBBL | 2017 | Instant | Any amount | 24×7 | Utility & recurring bills |

| 🛣️ NETC | NPCI | 2014 | Instant ⚡ | Toll amount | 24×7 (at tolls) | Highway toll payments |

| 🆔 AePS | NPCI+UIDAI | 2011 | Instant | Bank defined | BC hours | Rural banking, financial inclusion |

| 📄 CTS | RBI | 2013 | Same/next day | Cheque amount | Working days | Cheque clearance |

| 🏭 TReDS | RBI | 2017 | Within day | Invoice value | Working days | MSME invoice financing |

| 💳 PPI | RBI/PSOs | 2009+ | Instant | Up to ₹2L | 24×7 | Wallets, gift cards, prepaid |

| 🃏 Cards | NPCI/PSOs | 1990s+ | Instant | No fixed limit | 24×7 | Online/offline purchases |

🏛️ Who Controls India’s Payment Systems?

🔵 RBI Controls (Directly Owns & Operates)

- RTGS — directly owned and operated by RBI

- NEFT — owned and operated by RBI

- CTS — operated via CCIL (RBI subsidiary)

- TReDS — licensed and regulated by RBI

- Overall regulator of ALL payment systems in India

- Issues licences to PSOs (Payment System Operators)

- Sets rules under Payment & Settlement Systems Act, 2007

🟢 NPCI Controls (Operates Retail Systems)

- UPI — owned and operated by NPCI

- IMPS — owned and operated by NPCI

- NACH — operated by NPCI

- BBPS — via subsidiary NBBL (Bharat BillPay Ltd.)

- NETC — FASTag clearing operated by NPCI

- AePS — NPCI does switching & clearing

- RuPay Cards — NPCI’s own card network

🔴 Other PSOs (Licensed by RBI)

- Visa, Mastercard — international card networks (RBI licensed)

- PPI Issuers: Banks + Authorised non-banks (Paytm, etc.)

- Payment Aggregators: Razorpay, PayU, Cashfree

- Payment Gateways: CCAvenue, Instamojo

- These operate under RBI’s PSO licence

- Must comply with RBI regulations and NPCI standards

❓ Frequently Asked Questions

⚠️ Disclaimer

This blog is for informational and educational purposes only. All data about India’s payment systems has been sourced from official RBI publications, NPCI’s official website, the Payment and Settlement Systems Act 2007, RBI’s Half-Year Payment Systems Report (December 2024), Manorama Yearbook 2026, and verified financial research platforms as of April 2026.

- Transaction limits, charges, and availability of payment systems are subject to change by RBI/NPCI at any time. Always verify current limits on the official RBI website (rbi.org.in) or NPCI website (npci.org.in).

- The infographic used in this blog is attributed to RBI/NPCI educational materials and is used for informational purposes only.

- Paytm Payments Bank status reflects the situation as of April 2026 — Paytm UPI continues via partner banks. Always check official sources for the latest updates.

- This blog does not constitute financial or legal advice. For specific payment-related queries, contact your bank or RBI’s official helpline.